March 5, 2025

Jason N. Sheffield, J.D., National Director of Compliance.

Part One: Introduction

Respecting the ever-increasing liabilities assumed by plan sponsors and plan-level fiduciaries, enhanced regulatory scrutiny and agency enforcement protocols, as well as the frequency and ferocity of recent judicial interventions in the realm of fiduciary governance, it is more crucial than ever for employers sponsoring group health and welfare plans and programs to implement an organizational Health and Welfare Plan Fiduciary Committee.

This introductory guide outlines the basic structure, committee responsibilities, and organizational procedures underlying the creation and operation of a fiduciary committee in alignment with best practices to manage risk effectively while assuring legal and regulatory compliance.

Part Two: Purpose of the Fiduciary Committee

The Health and Welfare Plan Fiduciary Committee will be responsible for overseeing the administration and governance of the company’s health and welfare plans, programs, and related employee benefit offerings.

The committee’s primary objective is to ensure that plan operations adhere to fiduciary standards and the fiduciary code of conduct, as required by the Employee Retirement Income Security Act (“ERISA”) and its underlying Federal regulations.

Part Three: Operational Goals of the Committee

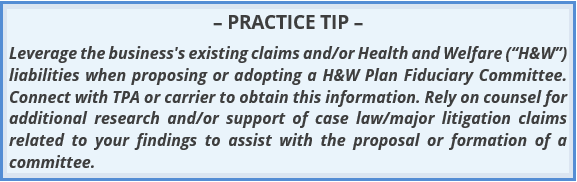

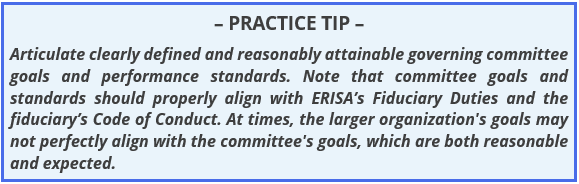

A primary responsibility of the governing organization is the establishment of the operational goals of the Fiduciary Committee. This is an important exercise because the scope of authorities and responsibilities charged to committee members will be a primary factor in the recruitment and retention of the committee’s membership. Further, a clearly and plainly articulated statement of purpose for the committee will help to ensure the committee is designed and operated for the sole and exclusive purpose of providing benefit to the plan participants and their eligible beneficiaries, as mandated by ERISA’s governing fiduciary obligations.

In addition, take heed of the following considerations when defining and articulating the committee’s operational goals:

- Compliance Assuredness: Ensure compliance with ERISA fiduciary duties and the Fiduciary’s Code of Conduct, as well as other relevant and/or applicable laws, regulations, and Federal agency guidance.

- Risk Mitigation: Purposefully and appropriately seek to mitigate legal liabilities and financial risks to health and welfare plans and programs via contemplation and memorializing clearly articulated and reasonably attainable committee goals.

- Prudent Governance: In developing the committee’s goals, remember that ERISA requires that plan-level fiduciaries act prudently, respecting their plan oversight responsibilities. This includes adherence to the Exclusive Purpose and the Plan Document Rules under ERISA (the former requiring plan fiduciaries to act solely in the interest of the plan’s participants and their beneficiaries, and the latter requiring that all plans and programs be administered in accordance with the written plan documents governing each plan or program).

- Governing Instruments: As the sponsoring organization, the committee’s statement of goals, as well as a clearly articulated statement of policy for the committee, serve as essential governing instruments for the operations of the committee. The statement of goals should incorporate clear and detailed instructions directing the committee on matters related to both accountability and oversight.

Part Four: Committee Structure

Generally, a Health and Welfare Plan Fiduciary Committee is comprised of specific delegated roles and responsibilities, though the exact composition of an individual organization’s specific committee will be largely dependent upon several factors, such as:

- Scope of Governance: Health and welfare plans and programs governed by the committee (consider also whether the committee will have authority respecting other benefit issues, such as executive compensation matters, retirement plans, ancillary benefit, etc.).

- Committee Composition and Size: The overall size of the committee, as well as role-specific functions and responsibilities.

- Appointment Tenure: Tenure of committee appointments.

- Goals & Responsibilities: A comprehensive inventory of the overarching committee goals, standards, and role specific responsibilities.

- Delegations of Authority: Written records and other archives respecting carrier, issuer, administrator, vendor, and engaged broker delegations of fiduciary liability and outlines of associated capabilities respecting the management of certain fiduciary functions.

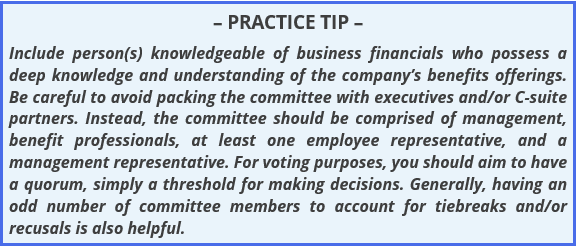

Notwithstanding the foregoing considerations, certain roles and responsibilities are always essential in committee development and formation, including:

- Committee Chair: Senior HR executive or benefits manager.

- Voting Committee Members: Representatives from the HR, finance, and legal departments.

- Committee Advisors (non-voting): External consultants, legal counsel, and auditors as needed.

- Secretary: Documents and maintains archives of the activities and votes of the operation committee.

Finally, remember that a committee should always have an odd number of members; this operates to avoid the occurrence of a tied vote. Also, in the event of a voting tie or irreconcilable opinions, the Committee Chair should always be authorized to submit tie-breaking votes and to redirect and/or table substantive discussion of any topic.

Part Five: Roles and Responsibilities

Committee roles and responsibilities also vary greatly depending upon individual and organizational preferences and the scopes of responsibilities and authorities granted to the committee; however, specific elemental roles and responsibilities are common to all fiduciary committees. These include items such as the following:

- Plan Oversight: Standards related to monitoring plan-level administration of health and welfare plans and programs to the satisfaction of ERISA and the plan sponsor’s authority as the plan settler of the plan or program.

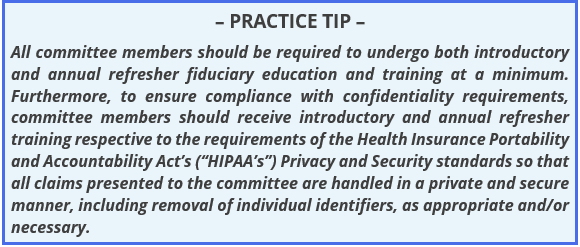

- Legal and Regulatory Compliance: All fiduciary committees should be delegated the authority and responsibility for legal and regulatory compliance assuredness. This extends beyond ERISA’s mandates and requirements to other relevant laws and regulations, such as HIPAA, MHPAEA, the ACA, and others.

- Adherence with ERISA Fiduciary Duties: Plan fiduciaries must act with prudence and in the best interests of the plan participants and beneficiaries. Fiduciaries are also charged to offset reasonable plan administration expenses and follow the terms of the underlying written plan documents.

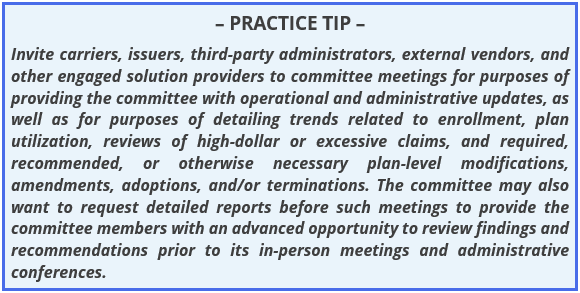

- Vendor Selection and Management: The committee should be responsible for monitoring vendors and service providers, including negotiation, design, and drafting of agreements and service contracts by and between service providers (including carriers, issuers, third-party administrators, vendors, and other third-party solution providers).

- Design, Adoption, and Maintenance of Participant Disclosures. The committee should oversee the production, dissemination, and maintenance of all required and supplemental participant disclosures, including plan documents, summary plan descriptions, material modifications, reduction summaries, plan amendments, Form 5500 filings, summary annual reports, summaries of benefits and coverage, and the like.

- Scheduling and Attending Required Meetings and Conferences: The committee should hold quarterly, monthly, or semi-monthly advisory meetings, as well as issue or topic sensitive ad hoc meetings as necessary to address non-routine or emergency matters. All meetings should be memorialized in writing (e.g., meeting minutes), with accountings of such archived for a period of seven years.

- Claims & Appeals: The committee should be designated as the appropriate adjudication body for the resolution of administrative and operational appeals and enrollee exceptions. This designation of authority should be memorialized in all underlying written participant disclosures, and such disclosures should be designed in an ERISA compliant manner, reserving for the plan fiduciaries the authority to provide final adjudication and/or final appeals in the instance of exceptions. Also, the committee should draft and adopt reasonable policies and procedures governing the resolution of all plan-level administrative exceptions.[1]

Part Six: Fiduciary Best Practices

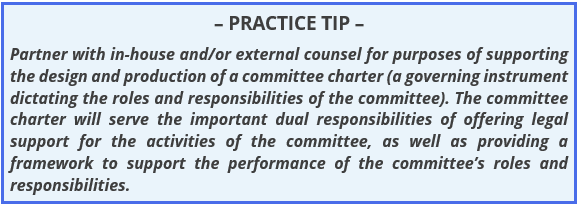

Design the committee charter in a reasonable and concise manner to provide for accurate and timely performance of required legal, regulatory, and governance activities, such as:

- Training: Provide ongoing fiduciary training for committee members to stay informed, respecting the current and evolving states of laws and regulations governing the committee standards of governance and performance.

- Documentation: Ensure that all committee activities are properly recorded in a written record of committee actions and activities, including meeting minutes, voting activities, appeals adjudications, and committee appointment and removal activities.

- Conflict of Interest Policy: Implement and enforce policies to identify and mitigate potential conflicts of interest (e.g., committee member recusal should they be privy to proprietary information concerning a particular matter or have an established relationship with a participant whose matter is before the committee).

- Monitoring, Oversight, and Auditing Functions: Conduct regular internal audits and seek independent assessments as needed to verify plan operations, including governance related and general plan administration guidance.

Part Seven: Risk Mitigation Strategies

One of the committee’s primary objectives is mitigating risk related activities and outcomes. Risk mitigation strategies involve both internal and external reviews, audits, and corrective measures. Some common risk mitigation related activities a committee may be charged to conduct include each of the following activities:

- Compliance Reviews and Audits: Conduct annual reviews of plan governance and administrative operations to ensure adherence to regulatory requirements and ongoing modifications of law, regulation, and organizational governance.

- Committee Insurance & Bonding: Securing fiduciary liability insurance and/or appropriate fiduciary bonds to protect committee members and organizational leadership against the effects and outcomes arising from successful allegations of nonfeasance and/or inadvertent mistake and the like. Remember that fiduciary liability insurance and fiduciary bonds do not generally compensate an organization in the event of a fiduciary’s malfeasance in the performance of professional duties, so the education of the committee should always be a central tenant of the legal functioning of the committee.

- Participant Communications: The committee should be charged to assure the timely, accurate, and transparent communication of plan-level benefits, rights, and features to plan participants and their enrolled beneficiaries, including, without limitation, plan-level adoptions, amendments, reductions, and terminations of plans and benefits (e.g., plan amendments, SMMs, SMRs, terminations, adverse benefit determinations, adverse appeals activities, provider communications and production requests, other benefit related adjudications, etc.).

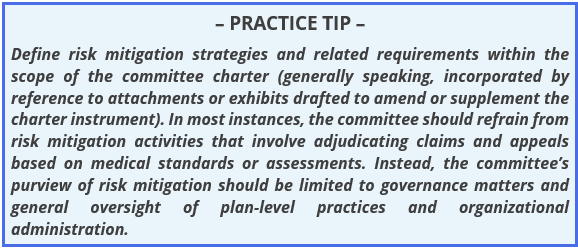

- Service Provider Engagements: The committee may review and engage independent review organizations (“IROs”) for external review and adjudication of claims and appeals (generally speaking, excluding final appeal determinations, committee members should refrain from making decisions regarding benefit claims and appeals based on medical determinations, such as necessity. Instead, they should collaborate with third-party administrators (“TPAs”), carriers, issuers, and other engaged professional service providers to ensure the initial and final appeal processes are followed). If necessary, the committee may seek to engage the services and expertise of an IRO for purposes of adjudication of second/final-level appeals.

Part Eight: Implementation Plan

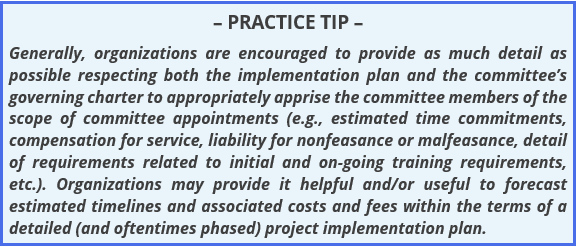

The charter and the committee’s related governing policies and procedures should outline the development and design of the organization’s committee implementation plan. The implementation plan is generally initiated through drafting and adopting a written action of the board of directors. At a minimum, the implementation plan should detail the following elements:

- Action of the Board of Directors: An action of the board of directors is the preferred implementation mechanism for a fiduciary committee. This document infers necessary authorities to the committee, as required for governance of the organization’s employee benefit plans.

- Identification of Initial Committee Composition: The implementation plan should identify, by name and by title, the initial composition of the committee; thereafter, committee changes should be handled in accordance with the provisions of the committee’s written charter.

- Initial Meeting: The implementation plan should designate the date, time, and location of the committee’s inaugural meeting; thereafter, committee meetings should be scheduled/dictated in accordance with the provisions of the committee’s written charter.

- Member Orientation and Initial Training: The implementation plan should account for the orientation of initial committee members and detailed requirements related to their initial training, whether by internal or external resources or engaged independent solution providers.

- Operational Launch: The implementation plan should detail a launch date for the committee’s oversight obligations, including activation of the committee charter.

Part Nine: Evaluation and Continuous Improvement

The committee should be charged with the performance of periodic and/or annual performance reviews and analyses. This is accomplished through the design, drafting, and adoption of operational policies and procedures governing the anticipated and expected activities of the committee. This includes policies and procedures related to the review of committee performance, including opportunities for service enhancements and/or improvement of governance activities. Annual reports summarizing the committee’s activities, findings, and recommendations should be presented to the executive and key leadership no less frequently than on an annual basis.

Part Ten: Approvals

Health & Welfare Plan Fiduciary Committees require the endorsement of senior leadership and relevant key stakeholders. Consequently, upon contemplation of the implementation of the committee, senior executives and key leadership should also be provided with adequate orientation and reasonable fiduciary education so that organizational decision-makers understand the necessity for the committee, as well as the scope of authorities and responsibilities conferred upon the committee.

Part Eleven: Summary & Conclusion

Establishing a Health and Welfare Plan Fiduciary Committee demonstrates an organization’s commitment to regulatory compliance, risk management, and protecting plan participants and beneficiaries. However, absent adequate planning, improper conferrence of responsibilities and authorities, and reasonable oversight mechanisms, a committee may cause more harm than good. For these and other reasons, it is imperative that the committee operate in accordance with an appropriate implementation plan and committee charter.

Furthermore, note that federal and state-level courts have been shown to demonstrate significant deference to the determinations of these types of governing committees upon the evaluation of and the balancing of equities arising in the adjudication of employee benefit-related claim disputes. To that end, a well-designed, properly trained, and successfully oriented fiduciary committee has the potential to ensure an organization’s successful administration of employee benefit-related obligations, respecting both regulatory obligations and overall participant satisfaction.

Through diligent and scope-appropriate implementation of an employee benefits fiduciary committee, a sponsoring organization may circumvent inherent risks and unnecessary liabilities while enhancing the benefit-related options and outcomes for participating employees and their enrolled dependents and beneficiaries.

Part Twelve: Topical Resources

The following topical federal agency resources and instructive materials may prove useful to organizations evaluating or implementing an employee benefit fiduciary committee:

- Fiduciary Responsibilities | U.S. Department of Labor

- Plan Administration and Compliance | U.S. Department of Labor

- Fulfilling Your Fiduciary Responsibilities

- Meeting Your Fiduciary Responsibilities | U.S. Department of Labor

- Employee Benefits Security Administration | U.S. Department of Labor

- A plan sponsor’s responsibilities | Internal Revenue Service

- Have you had your retirement plan checkup this year? | Internal Revenue Service

- Correcting plan errors | Internal Revenue Service

- Tax consequences of plan disqualification | Internal Revenue Service

- Employee benefits | Internal Revenue Service

- Retirement plan fiduciary responsibilities | Internal Revenue Service

For additional information or to obtain access to the Baldwin Group’s range of advisory solutions and support capabilities related to ERISA fiduciary status and the related fiduciary and settlor obligations, including adoption, oversight, and administration of a Health and Welfare Fiduciary Committee, please contact the Baldwin Group.

[1] Administrative exceptions and claims/appeals are distinguished by the fact that exceptions arise where the plan makes a fiduciary or settlor determination to permit of deny a claim or appeal on non-medical grounds, such as a change of organizational policy or administration, grandfathering of eligibility, one-off coverage or benefit exceptions, etc. However, adjudication of initial and final claims/appeal on medical grounds are generally made by carriers, issuers, third-party administrators, and other engaged third parties.

For more information

We’re ready when you are. Get in touch and a friendly, knowledgeable Baldwin advisor is prepared to discuss your business or individual needs, ask a few questions to get the full picture, and make a plan to follow up.

This document is intended for general information purposes only and should not be construed as advice or opinions on any specific facts or circumstances. The content of this document is made available on an “as is” basis, without warranty of any kind. The Baldwin Insurance Group Holdings, LLC (“The Baldwin Group”), its affiliates, and subsidiaries do not guarantee that this information is, or can be relied on for, compliance with any law or regulation, assurance against preventable losses, or freedom from legal liability. This publication is not intended to be legal, underwriting, or any other type of professional advice. The Baldwin Group does not guarantee any particular outcome and makes no commitment to update any information herein or remove any items that are no longer accurate or complete. Furthermore, The Baldwin Group does not assume any liability to any person or organization for loss or damage caused by or resulting from any reliance placed on that content. Persons requiring advice should always consult an independent adviser.

The Baldwin Group offers insurance services through one or more of its insurance licensed entities. Each of the entities may be known by one or more of the logos displayed; all insurance commerce is only conducted through The Baldwin Group insurance licensed entities. This material is not an offer to sell insurance.